Last spring, I sat down with a cup of coffee and pulled up my credit report for the first time in two years. I expected a clean slate. Instead, I found a credit card account I had closed five years ago still marked as open, and a late payment on a car loan I had paid off early. Neither was accurate. That morning cost me three hours, a few phone calls, and a lot of frustration—but it saved me from a higher mortgage rate down the road.

If you have never read your credit report closely, or if it has been a while, you are not alone. Most people only look when they are about to buy a house or finance a car. By then, an error can cost you real money. The good news? Reading a credit report is not as intimidating as it looks, and spotting mistakes is something anyone can learn to do.

Quick Fact: Under federal law, you can get a free copy of your credit report from each of the three major bureaus every week at AnnualCreditReport.com. This is the only official site authorized by federal law.

What Exactly Is a Credit Report?

A credit report is a detailed record of your borrowing and repayment history. It is compiled by three nationwide credit reporting agencies—Equifax, Experian, and TransUnion—and sold to lenders, landlords, insurers, and sometimes employers to evaluate your financial reliability.

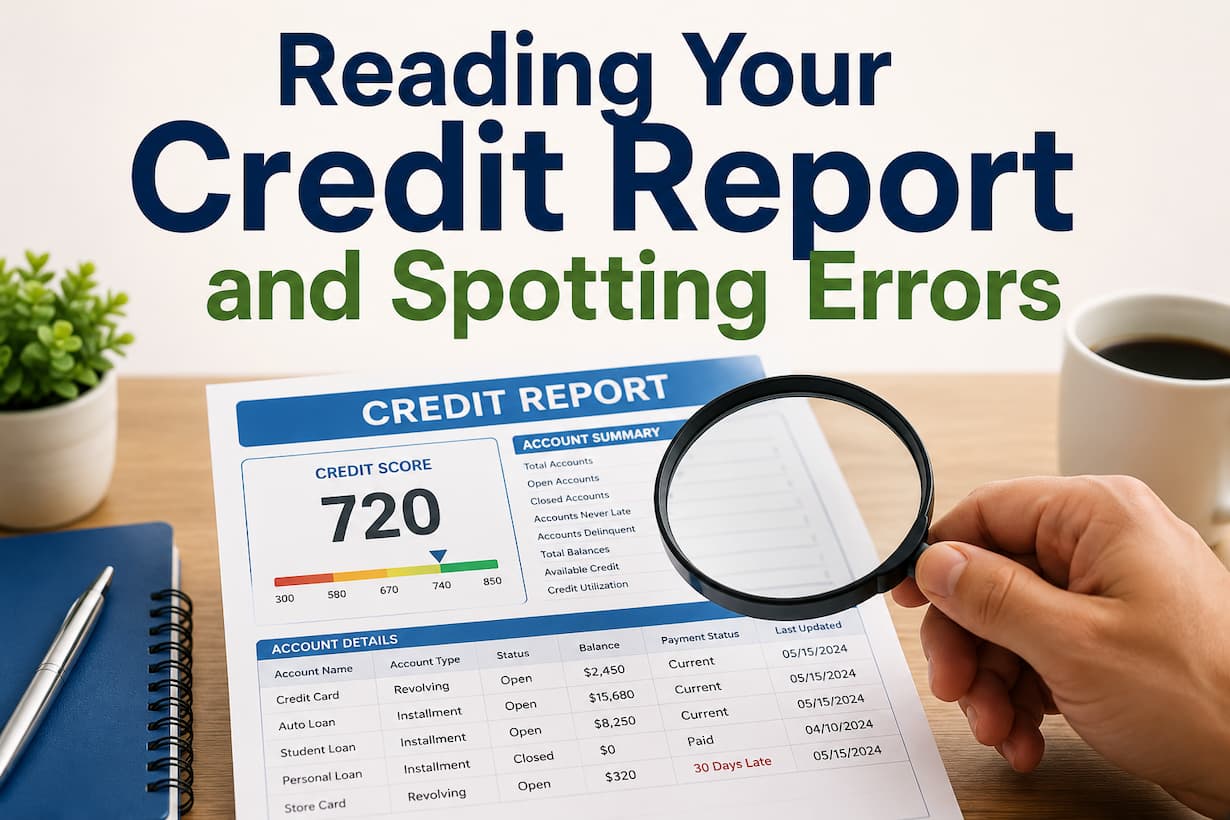

Your report is not a single score. It is a multi-page document broken into sections. Understanding each section is the first step toward catching errors before they damage your creditworthiness.

Breaking Down the Four Main Sections

Every credit report follows roughly the same structure. Here is what you will see and what to check in each area.

1. Personal Information

This section lists your name, current and former addresses, Social Security number, date of birth, and sometimes employers. It seems harmless, but a wrong middle initial or an old address linked to someone else with a similar name can cause your file to get mixed with theirs. I once saw a report in which a man’s file had been merged with his father’s because they shared the same name and lived at the same address, decades apart.

Red Flag: If you see addresses where you have never lived, names you do not recognize, or an incorrect Social Security number, treat it as a potential sign of identity theft or a mixed file.

2. Credit Accounts (Tradelines)

This is the meat of your report. It lists every credit card, mortgage, auto loan, student loan, and line of credit in your name. For each account, you will see the date opened, credit limit or loan amount, current balance, payment history, and account status (open, closed, in collections).

| What to Check | Why It Matters |

|---|---|

| Accounts you did not open | Strong indicator of identity theft or mixed files |

| Closed accounts showing as open | Inflates your available credit and can affect debt-to-income ratios |

| Duplicate entries for the same account | Makes your debt load appear larger than it is |

| On-time payments marked late | Payment history is the single biggest factor in your credit score |

| Incorrect credit limits | Skews your credit utilization ratio, which impacts scoring |

| Authorized user listed as primary owner | You may be held responsible for debt you never agreed to |

3. Public Records

This section includes bankruptcies, foreclosures, tax liens, and civil judgments. These items carry heavy weight and can stay on your report for seven to ten years. Check dates carefully. A bankruptcy that should have dropped off after ten years can linger and unfairly drag down your score.

4. Credit Inquiries

There are two types. Hard inquiries happen when you apply for credit and can slightly lower your score. Soft inquiries occur when you check your own report or when lenders pre-screen you for offers; these do not affect your score. If you see hard inquiries from companies you never contacted, that is a problem worth investigating.

Pro Tip: Hard inquiries stay on your report for two years but only affect your FICO score for the first 12 months. If you spot an unauthorized hard inquiry, dispute it immediately.

The Most Common Errors and What They Look Like

Errors are more common than most people assume. A study by the Federal Trade Commission found that one in five consumers had an error on at least one of their three credit reports. Here are the mistakes that show up most often.

Identity mix-ups. When two people share a name, live at the same address, or have similar Social Security numbers, their files can merge. You might see someone else’s mortgage or credit card on your report.

Outdated information. Negative items like late payments or collections are supposed to drop off after seven years. Bankruptcies after ten. Sometimes they do not.

Balance and limit errors. Your creditor might report a $5,000 balance when you actually owe $500, or list a $10,000 credit limit as $5,000. Either mistake can spike your credit utilization and hurt your score.

Re-aged debt. A collection agency might illegally reset the clock on an old debt, making it look newer than it is. This is against the Fair Credit Reporting Act.

Status mistakes. An account you paid off might still show as delinquent. An account in good standing might show as charged off. These are not just annoying—they can cost you thousands in higher interest.

Serious Warning: If you see an account you do not recognize, do not assume it is a harmless clerical error. Check your other reports. If the same unknown account appears across all three, freeze your credit immediately and file an identity theft report at IdentityTheft.gov.

How to Dispute an Error Step by Step

Finding the error is half the battle. Fixing it takes persistence. The Fair Credit Reporting Act gives you the right to dispute inaccurate information, and the credit bureaus are required to investigate within 30 days.

Here is the process that works.

Step 1: Gather your evidence. Do not just say something is wrong. Prove it. Collect bank statements, payment confirmations, court documents, or letters from your lender. Make copies. Never send originals.

Step 2: File with the credit bureau. You can dispute online, by phone, or by mail. Mail is slower, but it creates a paper trail. Send your dispute by certified mail with a return receipt requested. Include a clear explanation of the error, copies of your supporting documents, and a copy of your credit report with the error circled.

Step 3: File with the information furnisher. This is the bank, lender, or collection agency that reported the bad data to the bureau. Send them the same evidence and ask them to correct their records. If they verify that the information is wrong, they must notify all three bureaus.

Step 4: Wait and follow up. The bureau has 30 days to investigate. They will forward your evidence to the furnisher, who must investigate and report back. When the investigation ends, the bureau must send you written results and a free updated copy of your credit report if a change was made.

Step 5: Escalate if needed. If the bureau rejects your dispute or the error reappears, you have options. You can file a complaint with the Consumer Financial Protection Bureau, add a 100-word consumer statement to your report explaining the dispute, or consult a consumer protection attorney.

Important: If a credit bureau deems your dispute “frivolous,” they must tell you why within five business days. This usually happens when a dispute is too vague or lacks supporting evidence. Be specific and thorough in your initial filing.

How Often Should You Check?

The old advice was once a year. That is no longer enough. With free weekly reports available, checking quarterly is a reasonable minimum. I check mine every four months, rotating through one bureau at a time. That way I am always looking at a fresh report without pulling all three at once.

Check more frequently if you are:

- Planning to apply for a mortgage or car loan within the next six months

- Recovering from identity theft

- Actively disputing an error

- Recently divorced or separated, since joint accounts can create confusion

- About to start a job search in a field where employers check credit

Remember: Checking your own credit report is a soft inquiry and never hurts your score. Do not let fear of a temporary dip stop you from monitoring your financial health.

Frequently Asked Questions

1. Can I dispute an error online, or do I have to mail a letter?

You can do either. Online disputes are faster but offer less flexibility for attaching detailed explanations. Mailed disputes create a paper trail and are generally recommended for complex errors. The Consumer Financial Protection Bureau provides a sample dispute letter you can adapt.

2. How long does a dispute take to resolve?

Credit bureaus must complete their investigation within 30 days of receiving your dispute. If you submit additional documents during the investigation, the timeline may be extended to 45 days.

3. What if the bureau says the information is accurate and I still disagree?

You can request that a statement of your dispute be added to your file and included in future reports. You can also re-dispute with new evidence, file a complaint with the CFPB, or seek legal help.

4. Will disputing an error hurt my credit score?

No. The dispute process itself does not affect your score. If negative but accurate information is removed because it is outdated, your score may improve. If accurate negative information remains, your score will stay the same.

5. Do I need to pay a credit repair company to fix errors?

No. Everything a credit repair company can do, you can do yourself for free. Be cautious of companies that promise to remove accurate negative information or charge upfront fees. These are red flags for scams.

Bottom Line: Your credit report is one of the most important financial documents you own. No one cares about its accuracy more than you do. Set a reminder, pull your reports, read them carefully, and do not hesitate to challenge anything that looks wrong. The system is not perfect, but the law is on your side.

About this article: This guide was written to help everyday consumers understand and act on their credit reports without needing a finance degree. The information is based on current federal guidelines and industry practices as of 2026. It is not legal advice. If you are dealing with identity theft or repeated reporting violations, consider speaking with a qualified consumer protection attorney.

Sources and References

- Federal Trade Commission. “Disputing Errors on Your Credit Reports.” consumer.ftc.gov. Updated December 2025.

- Consumer Financial Protection Bureau. “How do I dispute an error on my credit report?” consumerfinance.gov. Updated December 2024.

- USA.gov. “Dispute errors on your credit report.” usa.gov. Updated November 2025.

- Equifax. “File a Dispute on Your Equifax Credit Report.” equifax.com.

- Schlanger Law Group. “How to Dispute Credit Report Errors: A 5-Step Guide.” consumerprotection.net. March 2026.

- Berger Montague. “3 Most Common Credit Report Errors.” bergermontague.com. November 2025.

Marcus Webb believes money advice should work for regular people, not just the already-wealthy. No Wall Street credentials or certified planner status — just years of researching financial strategies and sharing honest results, including the failures. Articles here are built on verifiable information and tested approaches, written to help readers navigate decisions without confusion or unnecessary complexity.