Homeownership comes with a quiet, persistent anxiety that renters rarely discuss. It’s the 2 AM worry about the furnace groaning through its twenty-third winter. The glance at the roof after every storm. The knowledge that somewhere behind a wall, water is slowly winning.

These aren’t hypotheticals. They’re certainties with unpredictable timing. A house doesn’t send calendar invites for its failures. But you can prepare for them without living in dread — or going broke when they arrive.

The 1% Rule: A Starting Point, Not Gospel

Conventional wisdom suggests setting aside 1% of your home’s value annually for maintenance and repairs. A $350,000 house means $3,500 yearly, or roughly $290 monthly. This rule is useful for budgeting, but it’s blunt.

A brand-new townhouse with a ten-year roof warranty and modern HVAC needs far less than a century-old Victorian with original plumbing and knob-and-tube wiring hiding in the walls. Location matters too. Coastal homes battle salt corrosion. Northern climates punish foundations with freeze-thaw cycles. Desert homes watch air conditioning systems die young under relentless sun.

Use the 1% rule as a floor, not a ceiling. Older homes, harsh climates, and properties with deferred maintenance history should push you toward 2–3%.

What I Learned the Hard Way: My first home was a 1960s ranch with “charming original features.” The charming original windows leaked air like a sieve. The charming original furnace died in February during a polar vortex. The emergency replacement cost $6,800 — triple what planned replacement would have run. I now budget 2.5% annually and sleep significantly better.

The Big-Ticket Items: When and How Much

Not all repairs are created equal. Some are annoyances. Others require loans. Knowing the typical lifespan and replacement cost of major systems lets you plan instead of panic.

| System / Component | Typical Lifespan | Replacement Cost Range | Warning Signs |

|---|---|---|---|

| Asphalt shingle roof | 20–25 years | $8,000–$25,000 | Curling shingles, granules in gutters, daylight through attic boards |

| HVAC system | 15–20 years | $5,000–$12,000 | Uneven heating, strange noises, rising energy bills, frequent cycling |

| Water heater | 8–12 years | $1,000–$3,500 | Rusty water, rumbling sounds, moisture around base, age sticker |

| Windows (full house) | 15–30 years | $5,000–$20,000 | Drafts, condensation between panes, difficulty opening/closing |

| Siding | 20–40 years | $6,000–$18,000 | Warping, cracking, rotting, fading, increased interior moisture |

| Driveway (asphalt) | 15–20 years | $3,000–$7,000 | Alligator cracking, potholes, drainage issues, faded color |

| Deck | 10–15 years (wood) | $4,000–$15,000 | Soft boards, loose railings, rot at posts, insect damage |

| Foundation repair | N/A (as needed) | $2,000–$15,000+ | Sticking doors, cracks in walls, sloping floors, water in basement |

Costs vary dramatically by region, material quality, and contractor availability. Get multiple quotes. Always.

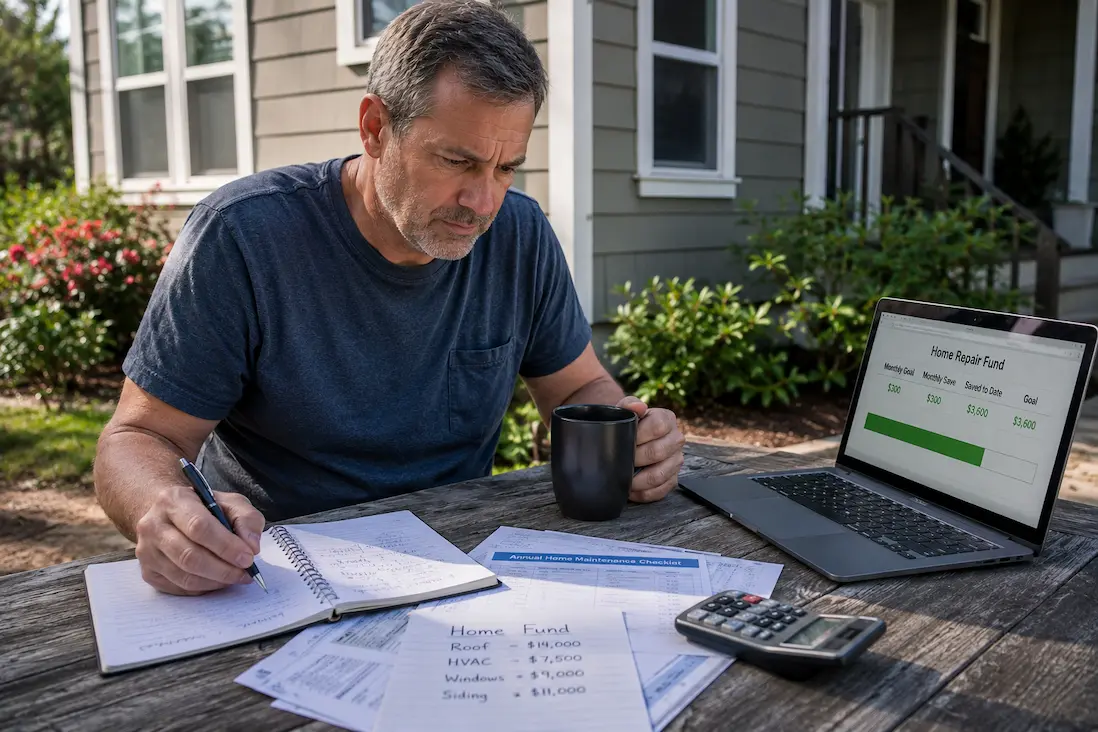

Building Your Home Repair Fund

Most people fund home repairs reactively — scrambling when something breaks. A smarter approach treats maintenance like a non-negotiable monthly bill, because it is.

Here’s a framework that actually works:

Open a dedicated high-yield savings account labeled “Home Fund.” Don’t mix it with vacation savings or your emergency fund. Mental accounting matters. When the money has a specific job, you’re less likely to borrow from it for non-home expenses.

Calculate your annual target using the 1–3% rule based on your home’s age and condition. Divide by twelve. Automate that transfer monthly. If you bought an older home or one with known issues, start higher and adjust after your first year of actual expenses.

When a repair comes in under budget, leave the surplus in the fund. Don’t celebrate with a dinner out. Home systems talk to each other, and they love failing in clusters. That $400 you saved on a plumber might cover the dishwasher that dies three weeks later.

Pro Tip: If you’re buying a home, negotiate a seller credit toward immediate repairs rather than asking for fixes. Contractors hired by sellers cutting corners to close are not your friends. Take the cash, hire your own people, and control quality.

The Maintenance Calendar Nobody Keeps (But Should)

Preventive maintenance is boring, unglamorous, and saves thousands. Most homeowners know this and still skip it because there’s no immediate payoff. Change that by scheduling it like dental cleanings.

Monthly: Check HVAC filters. Clean garbage disposal. Test smoke and carbon monoxide detectors. Inspect under sinks for leaks.

Quarterly: Clean dryer vent. Check exterior caulking around windows and doors. Flush water heater sediment. Inspect roof from ground for missing shingles or damage.

Twice yearly: Service HVAC professionally (spring and fall). Clean gutters. Inspect and clean refrigerator coils. Check outdoor faucets and sprinkler systems.

Annually: Professional roof inspection. Chimney sweep if you have a fireplace. Septic inspection if applicable. Water heater anode rod check. Deck structural inspection.

Yes, this list is long. No, you don’t need to do it all perfectly. But doing most of it most of the time catches problems when they’re $200 fixes instead of $5,000 emergencies.

When to DIY, When to Hire, When to Panic

Home improvement stores profit from your overconfidence. YouTube makes everything look achievable in a twenty-minute video with perfect lighting. Reality is messier.

Safe DIY: Painting interior walls. Replacing cabinet hardware. Caulking. Basic landscaping. Installing smart thermostats. Replacing faucet washers. These save labor costs and carry minimal risk of making things worse.

Hire a pro: Electrical work beyond swapping a light fixture. Gas line anything. Roof work (falls kill homeowners regularly). Structural modifications. Major plumbing behind walls. HVAC repairs. The money you “save” doing these yourself often becomes far more expensive when you need to hire someone to fix your fix.

Call immediately: Gas smell. Active water leak you can’t isolate. Electrical burning smell. Sagging ceiling (possible water damage). Foundation cracks that are widening. These aren’t projects. They’re emergencies that can destroy your home or harm your family.

Reality Check: I once watched a neighbor replace his own roof to save $8,000. He fell through a rotted section, broke his leg, and spent six weeks in a cast. The medical bills exceeded what he would’ve paid a crew. Some savings aren’t savings.

Insurance: What It Covers and What It Doesn’t

Homeowners insurance is not a maintenance fund. It’s for sudden, accidental damage — not wear and tear, not neglect, not gradual deterioration.

Your policy likely covers storm damage, fire, theft, and certain types of water damage (sudden pipe bursts). It almost certainly does not cover: slow leaks that rotted your subfloor over years, a roof that aged out of usefulness, termite damage, or mold from poor ventilation. Flood and earthquake coverage require separate policies entirely.

Read your declarations page. Understand your deductible. A $2,500 deductible means you’re self-insuring everything below that amount. Budget accordingly.

Financing Repairs When the Fund Falls Short

Even disciplined savers face surprises that outpace preparation. When that happens, know your options ranked by cost:

Best: Cash from your dedicated home fund. No interest, no debt.

Acceptable: Home equity line of credit (HELOC). Lower interest rates than personal loans or credit cards. Tax-deductible interest if used for home improvement. Risk: your home is collateral.

Last resort: Personal loans or credit cards. High interest, no tax benefit. Use only for genuine emergencies when no other option exists, and pay aggressively.

Avoid: payday loans, title loans, or contractor financing with deferred interest that balloons if not paid in full. These trap people in cycles that outlast the repair itself.

Related Articles

- How to Review and Update Your Financial Plan Yearly

- Protecting Your Family With the Right Emergency Fund

- How to Invest Small Amounts for Long-Term Growth

- Automating Your Savings for Consistent Growth

- Building a Household Budget That Everyone Can Follow

- How to Rework Your Budget After a Major Life Change

- How to Handle a Financial Windfall Responsibly

- Simple Methods to Lower Your Utility Costs Monthly

Sources and References

- HomeAdvisor. “True Cost Guide: Home Repair and Improvement Costs.” HomeAdvisor.com, 2024.

- Consumer Reports. “Home Maintenance Checklist.” ConsumerReports.org, January 2024.

- Insurance Information Institute. “What Does Homeowners Insurance Cover?” III.org.

- U.S. Department of Housing and Urban Development. “Looking for the Best Mortgage.” HUD.gov.

- National Association of Home Builders. “Housing Facts, Figures and Trends.” NAHB.org, 2023.

- Energy Star. “Maintenance Tips for Heating and Cooling Equipment.” EnergyStar.gov.

- Federal Trade Commission. “Home Equity Loans and Credit Lines.” Consumer.FTC.gov.

This piece was written after one too many conversations with friends blindsided by home repair bills they never saw coming. No certifications claimed — just a homeowner who learned that preparation beats panic, and that a little boring maintenance today prevents a lot of expensive chaos tomorrow.

Marcus Webb believes money advice should work for regular people, not just the already-wealthy. No Wall Street credentials or certified planner status — just years of researching financial strategies and sharing honest results, including the failures. Articles here are built on verifiable information and tested approaches, written to help readers navigate decisions without confusion or unnecessary complexity.